WHO WE ARE?

EGH is a globally driven company that is controlled, operated, managed, and directed by some of the world’s top iconic individuals—self-made millionaire and billionaire entrepreneurs—not just from the Middle East, but also from around the world.

WHAT DO WE DO?

The mission of “EGH” is to help almost any company succeed. Whether it’s a startup or an existing business that isn’t growing fast enough, EGH provides the tools and expertise to accelerate progress. EGH is an organization that focuses exclusively on acquiring, consulting, and preparing companies for major acquisitions or for going public (IPO). EGH achieves this by becoming directly involved in operations—structuring processes, raising funds, and enabling global expansion. EGH also specializes in guiding companies to go public, whether through a traditional IPO, a reverse merger, or a direct listing.

HOW DO WE DOIT?

The EGH team carefully evaluates every company to determine the best possible options as a consulting firm.

The EGH operating team—including the executive committee and board of directors—consists of individuals who are 100% committed and rated A+++ for professionalism, accuracy, intelligence, and involvement in global iconic ventures.

If Emerald Global Holdings LLC chooses to work with you—or allows you into their presence—it means you are truly blessed, both as an individual and as a company. You are sincerely the chosen one.

As the Chairman, Prince Fred, says:

“Ask me for money? You’ll get advice.

Ask me for advice? You’ll get money—twice!”

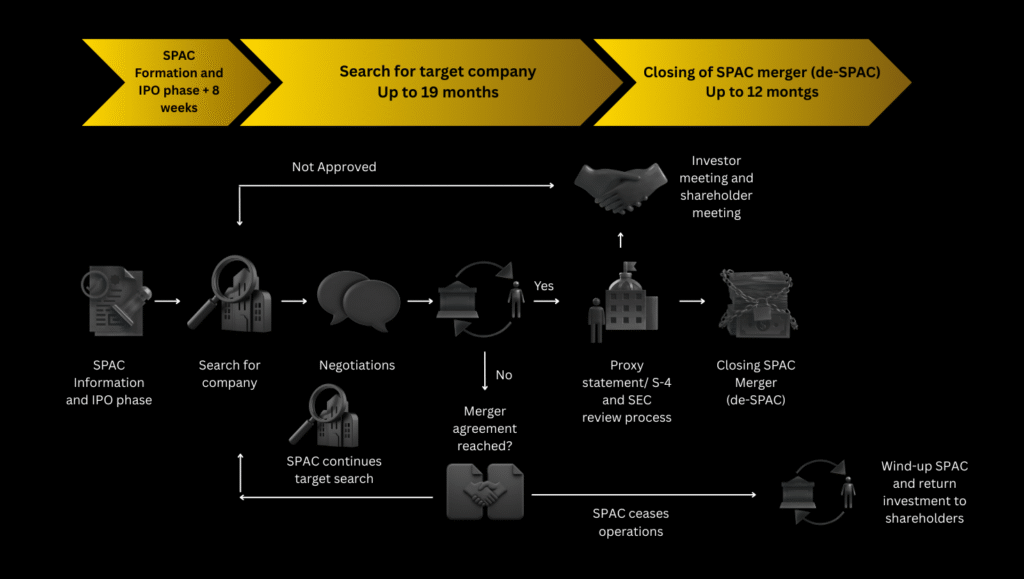

SPAC information & IPO phase

Search for company

Closing SPAC Merger (de-SPAC)

Merger agreement reached?

Wind-up SPAC & return investment to shareholders

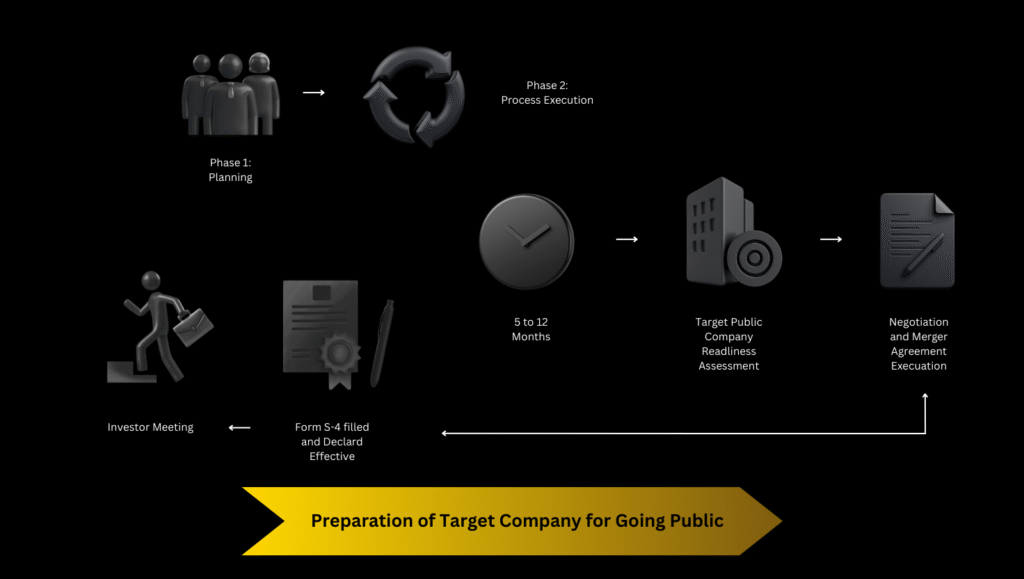

Phase 1: Planning

Phase 2: Process Execution

5 to 12 Months

Negotiation & Merger Agreement Execuation

Public company readiness

Project management

Tax structuring

SEC reporting accommodations

Financial statements

РСАОВ audits

Accounting acquirer

Pro formas

MD&A